Marriage changes how Medicaid works, but not in the way many people fear…

When couples begin researching Medicaid eligibility for married couples, the first reaction is often panic.

Someone hears that Medicaid requires you to “spend everything down,” and suddenly the questions start:

If my husband needs nursing home care, will I lose everything we’ve saved?

If I get married later in life, will I lose Medicaid benefits?

Can one spouse get Medicaid while the other keeps the house?

These are real concerns, and unfortunately, families often receive confusing or incomplete answers.

The good news is that Medicaid rules actually include protections designed specifically for married couples. In fact, federal Medicaid law includes provisions meant to prevent a healthy spouse from becoming impoverished simply because their partner needs long-term care.

Understanding how these rules work can make a significant difference in how families plan for care, protect assets, and maintain financial stability during a difficult time.

Why Medicaid treats married couples differently

When Medicaid was first created, policymakers quickly realized a major problem.

If one spouse required long-term care and Medicaid eligibility required the couple to spend down all their assets, the spouse still living at home could be left with virtually nothing.

To address this issue, spousal impoverishment protections were introduced into federal Medicaid law. These rules allow a married couple to qualify for Medicaid while still preserving certain resources for the spouse who remains in the community.

These protections are particularly important when one spouse enters a nursing home while the other continues living independently

More on 2026 Medicaid Eligibility in Kentucky here.

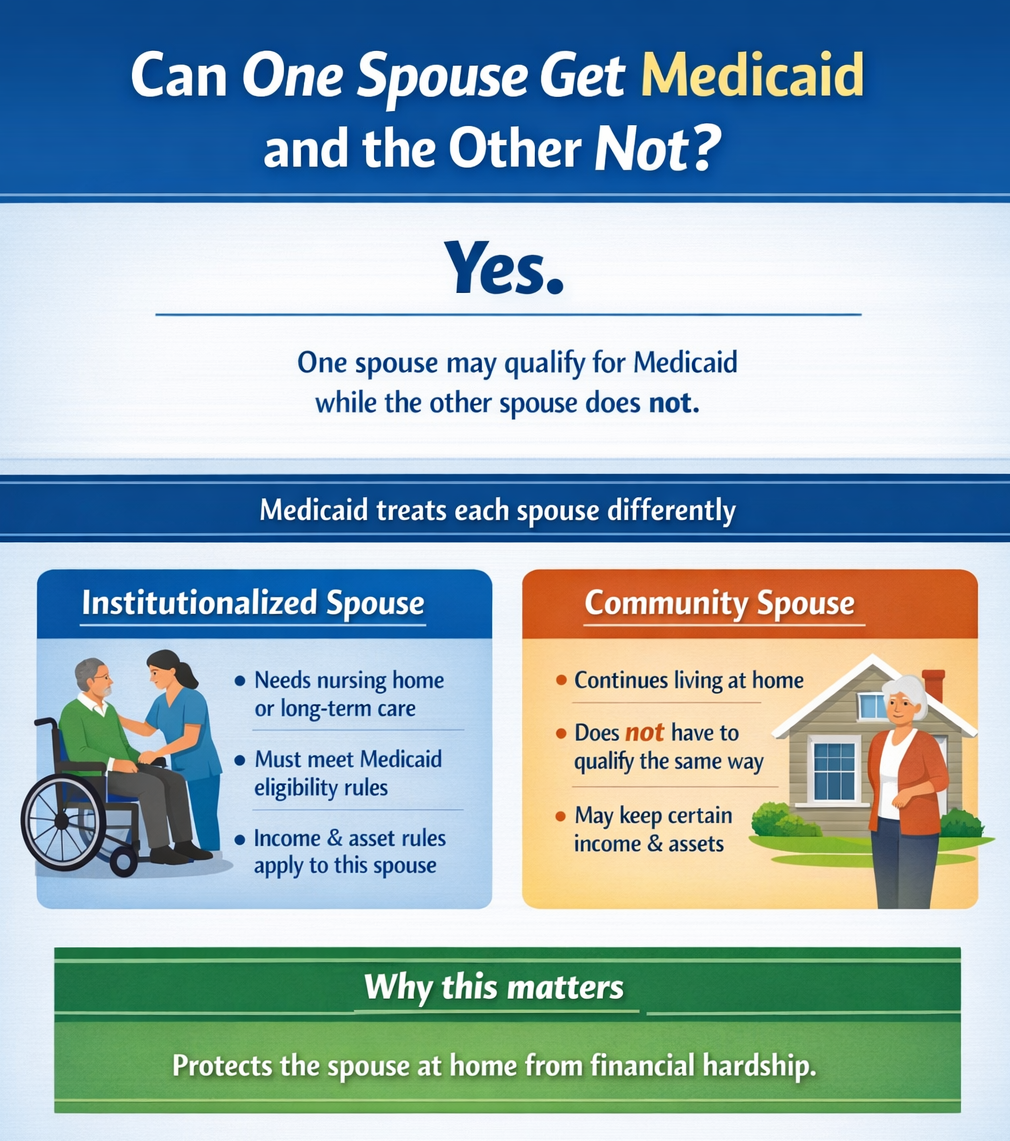

Can one spouse get Medicaid and the other not?

Yes. In many situations, one spouse may qualify for Medicaid while the other spouse does not.

When this happens, Medicaid divides the couple into two categories:

- Institutionalized spouse – the spouse who needs nursing home or long-term care

- Community spouse – the spouse who continues living at home

The financial rules for these two spouses are different.

The spouse receiving care must meet Medicaid eligibility requirements, while the spouse living at home is allowed to retain certain income and assets so they can continue living independently.

This distinction is one of the most important protections available to married couples navigating long-term care.

Will you lose Medicaid if you get married?

Another common concern is whether marriage itself will cause someone to lose Medicaid eligibility.

People often ask:

“If I get married will I lose Medicaid?”

The answer depends on the circumstances.

When someone receiving Medicaid marries, the state may begin evaluating the couple’s combined finances. In some cases, this can affect eligibility if the new spouse has significant income or assets.

However, Medicaid rules are designed to account for these situations. Eligibility is not automatically terminated simply because someone gets married.

Instead, the program examines the household finances to determine whether the combined resources still fall within Medicaid guidelines.

Because these situations can become complicated quickly, couples considering marriage later in life often benefit from reviewing their situation with an elder law attorney beforehand.

Income rules for married couples on Medicaid

When one spouse needs long-term care, Medicaid does not necessarily require all income to go toward the cost of care.

Instead, Medicaid’s spousal impoverishment rules protect the community spouse (the spouse who continues living at home). In 2026, the Minimum Monthly Maintenance Needs Allowance (MMMNA) is $2,705 per month in Kentucky, with a maximum MMMNA of $4,066.50 per month.

These protections may allow the community spouse to:

- retain enough monthly income to reach at least $2,705

- keep more income when shelter costs are high, up to $4,066.50

- benefit from a community spouse monthly housing allowance of $811.50 when calculating whether additional income should be protected for the spouse at home.

These rules are intended to help the spouse at home cover basic living expenses and avoid financial hardship while the other spouse receives care. For Medicaid in Kentucky, the community spouse income allowance is specifically capped at $4,066.50 effective January 1, 2026.

Asset protections for married couples

Assets are another major concern for couples exploring Medicaid eligibility.

When one spouse enters a nursing facility, Medicaid typically evaluates the couple’s combined assets to determine eligibility.

However, certain protections allow the community spouse to keep a portion of the couple’s assets.

These may include:

- The primary residence (in many cases)

- One vehicle

- Personal belongings

- Certain financial resources within allowable limits

The exact amount the community spouse may retain depends on several factors, including Kentucky guidelines and the couple’s financial situation.

Understanding how these rules apply is essential for avoiding unnecessary loss of savings or property.

What about the family home?

For many couples, the house represents both their largest financial asset and their emotional center.

Fortunately, in many situations the primary residence is protected while the community spouse continues living there.

However, the home may still become relevant later through Medicaid estate recovery, which allows the state to seek reimbursement from certain assets after the Medicaid recipient passes away.

This is why planning ahead can be particularly important when a home is involved.

More on this topic here: Can You Get Medicaid If You Own a Home?

Why planning ahead can make a significant difference

Couples often believe they must wait until a crisis occurs before considering Medicaid eligibility.

In reality, planning ahead can provide more options.

Early planning may allow families to:

- Protect assets more effectively

- Avoid unnecessary Medicaid penalties

- Ensure the community spouse remains financially secure

- Navigate eligibility rules more confidently

- Avoid the 5-year lookback

Waiting until a hospital discharge or nursing home admission can limit the available strategies and create additional stress for families already facing difficult decisions.

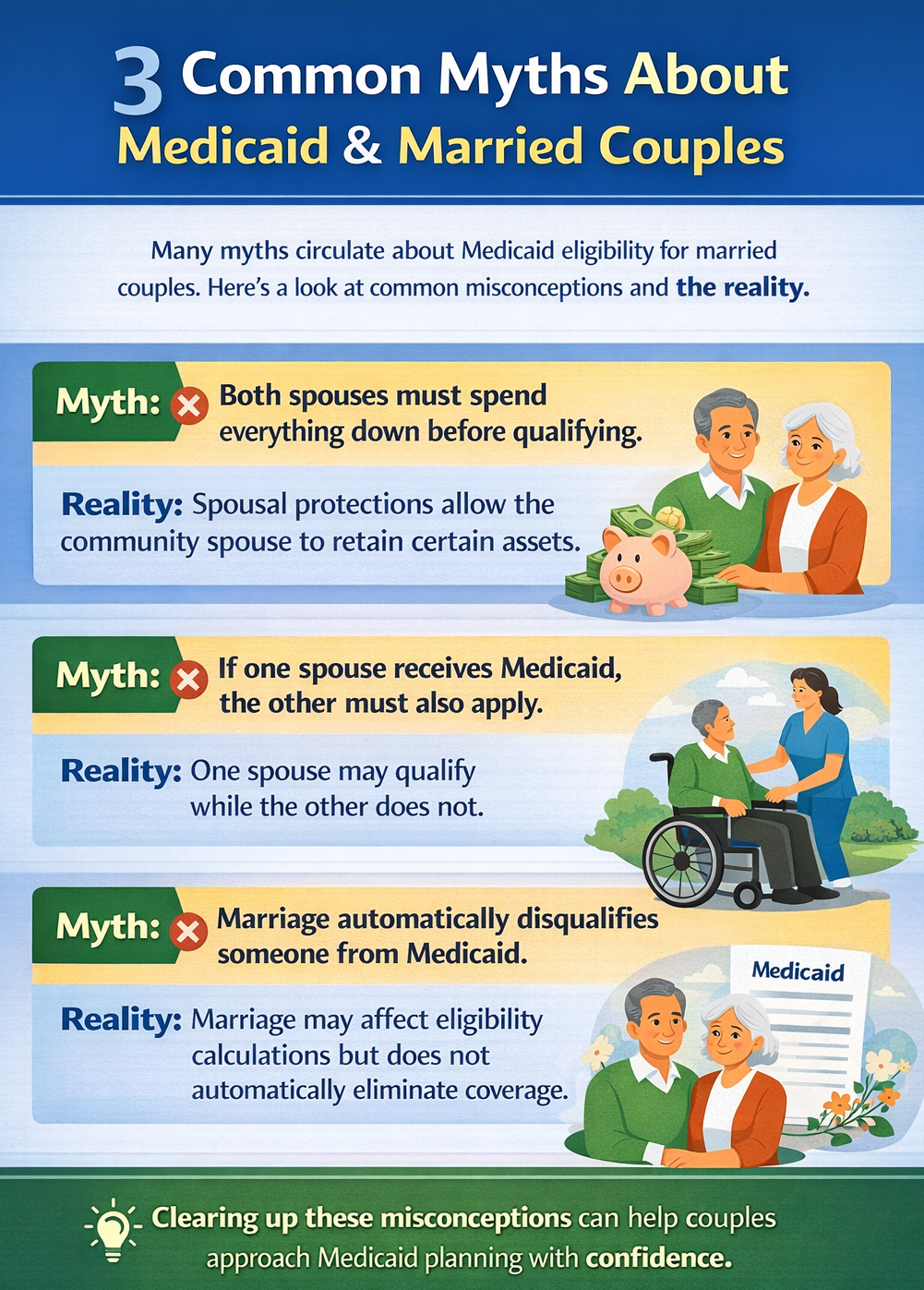

Common misunderstandings about Medicaid and marriage

Several myths continue to circulate about Medicaid eligibility for married couples.

Medicaid rules are designed to protect spouses, not punish them

For married couples, the idea of Medicaid often brings immediate anxiety about losing everything.

Fortunately, the program includes protections specifically designed to prevent the spouse living at home from being left without financial resources.

Understanding how Medicaid eligibility for married couples works can help families make informed decisions about care, finances, and planning.

Most importantly, knowing the rules ahead of time can help couples avoid unnecessary mistakes during what is often already a stressful period.

Talk with someone who understands Medicaid planning

If you and your spouse are exploring long-term care options or wondering how Medicaid eligibility might affect your finances, it can be helpful to review your situation with an elder law attorney who is familiar with the process.

Schedule a consultation with Elder Law Guidance today, and discuss with one of our experienced elder law attorney’s how Medicaid rules may apply to your family’s circumstances.

Understanding your options may help protect both your care and your financial stability in the future.